FAQ

About the Company

What is the stock code?

The Company's stock code (ticker) is 5027.

When did the company go public?

The Company went public on March 29, 2023.

What is the background of the company?

AnyMind Group was founded in Singapore in April 2016 and currently operates from 22 offices and locations across 15 markets worldwide. AnyMind Group is a technology company that provides a one-stop platform for solutions such as brand development, manufacturing management, media management, e-commerce enablement, marketing and logistics management.

What kind of business do you operate?

Enterprise Growth business:

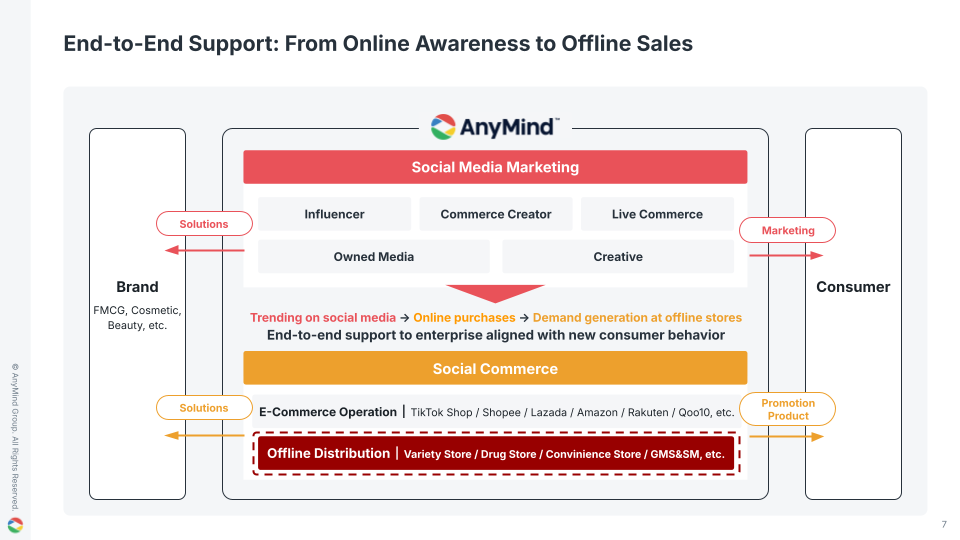

We develop e-commerce and marketing support platforms for enterprise clients and provide them in combination with operational support. We offer one-stop support covering everything from brand design and planning, production management, e-commerce site construction and operation, marketing, live commerce, and logistics management, to AI implementation and digital transformation. In our financial results, this business domain is disclosed under two segments: Marketing business and D2C/E-Commerce business.

Publisher Growth business:

We provide advertising revenue optimization and user acquisition support utilizing our platform for publishers operating web media and mobile applications.

Creator Growth business:

We provide comprehensive support for video creators and influencers to facilitate their activities, covering content monetization, sponsor acquisition, merchandise development, and management.

We develop e-commerce and marketing support platforms for enterprise clients and provide them in combination with operational support. We offer one-stop support covering everything from brand design and planning, production management, e-commerce site construction and operation, marketing, live commerce, and logistics management, to AI implementation and digital transformation. In our financial results, this business domain is disclosed under two segments: Marketing business and D2C/E-Commerce business.

Publisher Growth business:

We provide advertising revenue optimization and user acquisition support utilizing our platform for publishers operating web media and mobile applications.

Creator Growth business:

We provide comprehensive support for video creators and influencers to facilitate their activities, covering content monetization, sponsor acquisition, merchandise development, and management.

I would like to know the details regarding the increase in employee numbers in fiscal year 2025.

Disclosed on February 13, 2026

Our employee count at the end of fiscal year 2025 was 2,163, an increase of 220 people, or approximately 11%, from the end of fiscal year 2024. The breakdown is 86 people from M&A and 134 people from organic growth. By quarter, we had an increase of 92 people in the first quarter, 12 people in the second quarter, 66 people in the third quarter, and 50 people in the fourth quarter.

The first quarter coincided with the period when changes in the external environment surrounding the Creator Growth Business occurred, but at that time, we were proceeding with hiring based on the recruitment plan formulated at the beginning of the fiscal year, on the premise of maintaining a certain personnel buffer in each business. Subsequently, in light of changes in the external environment, we revised our recruitment policy from the second quarter onwards, shifting to more disciplined hiring while still assuming investment in growth areas.

Breaking down the factors for the personnel increase, first regarding the impact of M&A, we executed three M&A deals in fiscal year 2025: an increase of 8 people in the first quarter due to the consolidation of AnyReach in March, an increase of 73 people in the third quarter due to the consolidation of Vibula in September, and an increase of 5 people in the fourth quarter due to the consolidation of NADESHIKO in October.

On the other hand, on an organic basis excluding M&A, the increase in the fourth quarter is relatively large, which is mainly due to strengthening personnel centered on the enterprise e-commerce support area, which has been performing well.

To achieve our medium-term targets, we position the improvement of business efficiency through the utilization of AI as an important premise, and it is currently progressing largely according to plan. We expect full-scale contribution to business performance from fiscal year 2026 onward, with productivity improvements expected to appear more significantly toward the latter half of the medium-term target period.

While there is a possibility of personnel increases due to M&A in fiscal year 2026 as well, our policy is to restrain organic personnel increases and achieve business growth through productivity improvement. Going forward, we will aim to achieve our medium-term targets while balancing personnel investment in growth areas with business efficiency improvements.

Our employee count at the end of fiscal year 2025 was 2,163, an increase of 220 people, or approximately 11%, from the end of fiscal year 2024. The breakdown is 86 people from M&A and 134 people from organic growth. By quarter, we had an increase of 92 people in the first quarter, 12 people in the second quarter, 66 people in the third quarter, and 50 people in the fourth quarter.

The first quarter coincided with the period when changes in the external environment surrounding the Creator Growth Business occurred, but at that time, we were proceeding with hiring based on the recruitment plan formulated at the beginning of the fiscal year, on the premise of maintaining a certain personnel buffer in each business. Subsequently, in light of changes in the external environment, we revised our recruitment policy from the second quarter onwards, shifting to more disciplined hiring while still assuming investment in growth areas.

Breaking down the factors for the personnel increase, first regarding the impact of M&A, we executed three M&A deals in fiscal year 2025: an increase of 8 people in the first quarter due to the consolidation of AnyReach in March, an increase of 73 people in the third quarter due to the consolidation of Vibula in September, and an increase of 5 people in the fourth quarter due to the consolidation of NADESHIKO in October.

On the other hand, on an organic basis excluding M&A, the increase in the fourth quarter is relatively large, which is mainly due to strengthening personnel centered on the enterprise e-commerce support area, which has been performing well.

To achieve our medium-term targets, we position the improvement of business efficiency through the utilization of AI as an important premise, and it is currently progressing largely according to plan. We expect full-scale contribution to business performance from fiscal year 2026 onward, with productivity improvements expected to appear more significantly toward the latter half of the medium-term target period.

While there is a possibility of personnel increases due to M&A in fiscal year 2026 as well, our policy is to restrain organic personnel increases and achieve business growth through productivity improvement. Going forward, we will aim to achieve our medium-term targets while balancing personnel investment in growth areas with business efficiency improvements.

Regarding the control of hiring, please explain how you will balance this with business growth.

Disclosed on October 1, 2025

To achieve both business growth and profitability, we are currently taking a balanced approach to our hiring activities, tailoring them to the situation of each business.

Specifically, in our operational delivery and corporate departments, the increase in personnel is being controlled on the premise of improving operational efficiency, including through the use of AI. On the other hand, we are continuing strategic hiring for front-office roles (sales and business development) in our growth businesses, as well as in our product development division, centered on the areas necessary to achieve our business plan. Furthermore, we are also working on the optimal allocation of existing personnel and promoting inter-departmental transfers based on aptitude, thereby striving to maximize the utilization of our internal human resources.

By improving productivity through this optimization of hiring and maximization of internal resources, we aim to achieve revenue growth from the next fiscal year onwards while controlling the increase in our number of employees.

To achieve both business growth and profitability, we are currently taking a balanced approach to our hiring activities, tailoring them to the situation of each business.

Specifically, in our operational delivery and corporate departments, the increase in personnel is being controlled on the premise of improving operational efficiency, including through the use of AI. On the other hand, we are continuing strategic hiring for front-office roles (sales and business development) in our growth businesses, as well as in our product development division, centered on the areas necessary to achieve our business plan. Furthermore, we are also working on the optimal allocation of existing personnel and promoting inter-departmental transfers based on aptitude, thereby striving to maximize the utilization of our internal human resources.

By improving productivity through this optimization of hiring and maximization of internal resources, we aim to achieve revenue growth from the next fiscal year onwards while controlling the increase in our number of employees.

Please tell us about your human resources strategy and the current recruitment situation.

Disclosed on October 1, 2024

Our human resources strategy is characterized by its fusion of a global outlook with local characteristics. While we have dedicated recruitment teams at each location, we also have a team overseeing global HR strategy and crossborder recruitment. This structure allows us to balance recruitment activities that meet each country's specific needs with the execution of a consistent global strategy.

In terms of competitive advantage in talent acquisition, we have a unique presence as a startup originating from Southeast Asia. We have achieved high growth while maintaining stable profitability improvement and financial soundness, along with the credibility of being a listed company. Moreover, there are very few companies with such a multinational organization and culture. We maximize this unique position to strategically and efficiently attract talent in each country who are eager to build careers in the global internet industry.

We are also strengthening knowledge sharing and talent development. For example, we conduct company-wide monthly knowledge sharing sessions and cross-departmental reporting meetings to promote the horizontal expansion of best practices. Furthermore, we aim to broaden employees' global perspectives and deepen cross-cultural understanding through the promotion of cross-border projects. We also provide diverse and advanced learning opportunities, including AI-support training programs, an internal online learning platform, and level-specific training. Going forward, we aim to establish a sustainable growth foundation by developing flexible human resource strategies that respond quickly to rapid market and technological changes.

Our human resources strategy is characterized by its fusion of a global outlook with local characteristics. While we have dedicated recruitment teams at each location, we also have a team overseeing global HR strategy and crossborder recruitment. This structure allows us to balance recruitment activities that meet each country's specific needs with the execution of a consistent global strategy.

In terms of competitive advantage in talent acquisition, we have a unique presence as a startup originating from Southeast Asia. We have achieved high growth while maintaining stable profitability improvement and financial soundness, along with the credibility of being a listed company. Moreover, there are very few companies with such a multinational organization and culture. We maximize this unique position to strategically and efficiently attract talent in each country who are eager to build careers in the global internet industry.

We are also strengthening knowledge sharing and talent development. For example, we conduct company-wide monthly knowledge sharing sessions and cross-departmental reporting meetings to promote the horizontal expansion of best practices. Furthermore, we aim to broaden employees' global perspectives and deepen cross-cultural understanding through the promotion of cross-border projects. We also provide diverse and advanced learning opportunities, including AI-support training programs, an internal online learning platform, and level-specific training. Going forward, we aim to establish a sustainable growth foundation by developing flexible human resource strategies that respond quickly to rapid market and technological changes.

About Business

What specific impact will the advancement of AI have on your business?

Disclosed on April 3, 2026

We view the advancement of AI as an opportunity for growth and profitability improvement. There are three main reasons for this.

1. "Source of Value" Difficult to Replace with Generative AI and Resilient Demand

The sources of our competitiveness are our "proprietary data" accumulated over many years and our strong "sales capabilities and global network." In our core influencer business in particular, the personal reach and impact of individuals—driven by their distinct personalities and trusted relationships—constitute the fundamental value, which we believe is difficult for AI to replicate. Precisely because AI is evolving, the distinctive value of human involvement and execution capabilities is becoming even more pronounced, and demand for our services remains resilient.

2. Opportunities to Improve Operational Efficiency

In the Enterprise Growth business especially, operational workloads were traditionally heavy, requiring headcount increases in step with business growth, therefore, the recruitment burden and rising costs were challenges. However, areas such as data management present significant opportunities for AI-driven automation and efficiency gains. By applying our operational expertise to AI, we expect to achieve meaningful productivity improvements.

3. Opportunity Creation and Product Evolution Through AI Across Business Domains

Each business division is proactively responding to changes in the operating environment and pursuing new opportunities. We will build sustainable competitive advantages through AI-integrated service evolution, for example, by deploying a hybrid live commerce solution that combines our in-house generative AI live commerce platform, "AnyLive," with human live. In addition, we are adapting to shifts in market demand, such as strengthening mobile app support within the Publisher Growth domain, an area where near-term market growth is anticipated.

We view the advancement of AI as an opportunity for growth and profitability improvement. There are three main reasons for this.

1. "Source of Value" Difficult to Replace with Generative AI and Resilient Demand

The sources of our competitiveness are our "proprietary data" accumulated over many years and our strong "sales capabilities and global network." In our core influencer business in particular, the personal reach and impact of individuals—driven by their distinct personalities and trusted relationships—constitute the fundamental value, which we believe is difficult for AI to replicate. Precisely because AI is evolving, the distinctive value of human involvement and execution capabilities is becoming even more pronounced, and demand for our services remains resilient.

2. Opportunities to Improve Operational Efficiency

In the Enterprise Growth business especially, operational workloads were traditionally heavy, requiring headcount increases in step with business growth, therefore, the recruitment burden and rising costs were challenges. However, areas such as data management present significant opportunities for AI-driven automation and efficiency gains. By applying our operational expertise to AI, we expect to achieve meaningful productivity improvements.

3. Opportunity Creation and Product Evolution Through AI Across Business Domains

Each business division is proactively responding to changes in the operating environment and pursuing new opportunities. We will build sustainable competitive advantages through AI-integrated service evolution, for example, by deploying a hybrid live commerce solution that combines our in-house generative AI live commerce platform, "AnyLive," with human live. In addition, we are adapting to shifts in market demand, such as strengthening mobile app support within the Publisher Growth domain, an area where near-term market growth is anticipated.

What are your impressions of the TikTok Shop launch in Japan? When do you expect it to start contributing to financial results?

Disclosed on April 3, 2026

Given that TikTok Shop in Japan is still in its early stages, we believe its GMV (Gross Merchandise Volume) is tracking at a reasonable scale and pace of growth. It took approximately one to two years from launch to full-scale growth acceleration in both Southeast Asia and the United States, and we expect Japan to follow a similar growth trajectory. While 2025 was a trial phase, we anticipate a growing number of major brands entering the platform in 2026, and we see significant room for market expansion.

The contribution to our financial results is limited at this point, but we expect it to reach a meaningful scale toward the second half of 2026. In Southeast Asia, by contrast, TikTok Shop has already established itself as a major e-commerce sales channel in each market and is contributing meaningfully to our results.

Importantly, what we emphasize even more is not just standalone sales on TikTok Shop, but channeling the demand created on TikTok to other e-commerce platforms and offline sales. We provide integrated support for sales across multiple channels, including e-commerce marketplaces such as Amazon and Rakuten, as well as the offline distribution network operated by SUNSMILE.

In the cross-border domain in particular, our engagements are primarily structured on a GMV-linked revenue model, where we provide comprehensive operational support across sales channels and our revenue scales with transaction volume. This means our revenue growth is driven by sales expansion across multiple channels, rather than being dependent on any single channel.

We are currently building an integrated online-to-offline sales infrastructure, including through our collaboration with SUNSMILE.

Given that TikTok Shop in Japan is still in its early stages, we believe its GMV (Gross Merchandise Volume) is tracking at a reasonable scale and pace of growth. It took approximately one to two years from launch to full-scale growth acceleration in both Southeast Asia and the United States, and we expect Japan to follow a similar growth trajectory. While 2025 was a trial phase, we anticipate a growing number of major brands entering the platform in 2026, and we see significant room for market expansion.

The contribution to our financial results is limited at this point, but we expect it to reach a meaningful scale toward the second half of 2026. In Southeast Asia, by contrast, TikTok Shop has already established itself as a major e-commerce sales channel in each market and is contributing meaningfully to our results.

Importantly, what we emphasize even more is not just standalone sales on TikTok Shop, but channeling the demand created on TikTok to other e-commerce platforms and offline sales. We provide integrated support for sales across multiple channels, including e-commerce marketplaces such as Amazon and Rakuten, as well as the offline distribution network operated by SUNSMILE.

In the cross-border domain in particular, our engagements are primarily structured on a GMV-linked revenue model, where we provide comprehensive operational support across sales channels and our revenue scales with transaction volume. This means our revenue growth is driven by sales expansion across multiple channels, rather than being dependent on any single channel.

We are currently building an integrated online-to-offline sales infrastructure, including through our collaboration with SUNSMILE.

Is there any impact on financial results from the recent situation in the Middle East?

Disclosed on April 3, 2026

We operate in certain regions of the Middle East, and while the Marketing business in those regions has been partially affected by geopolitical conditions in the region, the impact on our consolidated financial results is limited.

The first quarter typically coincides with the Ramadan period in Muslim-majority markets, during which our Middle East business tends to grow alongside rising consumer demand. However, for the current fiscal year, seasonal demand growth has been softer than usual. That said, gross profit from the Middle East region represented less than 0.5% of total consolidated gross profit in FY2025, and the impact of the current situation is confined to a portion of our operations in the region.

In addition, while there are concerns that elevated crude oil prices could lead to higher logistics costs, such costs represent less than 1% of our cost of sales, and we do not anticipate any material impact at this time.

We operate in certain regions of the Middle East, and while the Marketing business in those regions has been partially affected by geopolitical conditions in the region, the impact on our consolidated financial results is limited.

The first quarter typically coincides with the Ramadan period in Muslim-majority markets, during which our Middle East business tends to grow alongside rising consumer demand. However, for the current fiscal year, seasonal demand growth has been softer than usual. That said, gross profit from the Middle East region represented less than 0.5% of total consolidated gross profit in FY2025, and the impact of the current situation is confined to a portion of our operations in the region.

In addition, while there are concerns that elevated crude oil prices could lead to higher logistics costs, such costs represent less than 1% of our cost of sales, and we do not anticipate any material impact at this time.

Please provide the outlook for the Enterprise Growth Business going forward.

Disclosed on February 13, 2026

We position the social commerce domain as the core of our medium- to long-term growth strategy, with the Enterprise Growth Business being central to it. In 2025, gross profit in this area achieved high growth at 31.5% year-over-year.

Our strength lies in our ability to provide integrated capabilities across Asia, from social media marketing to e-commerce support. In addition, by integrating technology, data, and operations in-house, we believe we are positioned to further solidify competitive advantages even in a market environment where AI adoption is advancing.

Marketing and commerce support, including e-commerce, are strongly connected in terms of customer data accumulation and upselling opportunities, and by combining them, we create synergies that enhance customer value and profitability. Furthermore, our publisher and creator networks function as strategic assets that support the sales expansion of enterprise brands, accelerating the overall growth of the Enterprise Growth Business.

In 2025, with the rapid expansion of enterprise e-commerce support, we prioritized operational structure and personnel development, which resulted in short-term resource constraints in some areas. However, organizational development is now progressing, and from 2026 onwards, we are establishing a foundation to grow both marketing and e-commerce in a balanced manner.

Going forward, we will continue to strengthen our social commerce support structure that integrates marketing and commerce support, aiming to sustain high growth over the medium to long term.

We position the social commerce domain as the core of our medium- to long-term growth strategy, with the Enterprise Growth Business being central to it. In 2025, gross profit in this area achieved high growth at 31.5% year-over-year.

Our strength lies in our ability to provide integrated capabilities across Asia, from social media marketing to e-commerce support. In addition, by integrating technology, data, and operations in-house, we believe we are positioned to further solidify competitive advantages even in a market environment where AI adoption is advancing.

Marketing and commerce support, including e-commerce, are strongly connected in terms of customer data accumulation and upselling opportunities, and by combining them, we create synergies that enhance customer value and profitability. Furthermore, our publisher and creator networks function as strategic assets that support the sales expansion of enterprise brands, accelerating the overall growth of the Enterprise Growth Business.

In 2025, with the rapid expansion of enterprise e-commerce support, we prioritized operational structure and personnel development, which resulted in short-term resource constraints in some areas. However, organizational development is now progressing, and from 2026 onwards, we are establishing a foundation to grow both marketing and e-commerce in a balanced manner.

Going forward, we will continue to strengthen our social commerce support structure that integrates marketing and commerce support, aiming to sustain high growth over the medium to long term.

Please explain the status and future outlook for the Creator Growth Business.

Disclosed on February 13, 2026

Regarding the Creator Growth Business in fiscal year 2025, and as a result of changes in the external environment, gross profit was 2.64 billion yen, a decrease of 22.5% year-over-year.

In light of this situation, to strengthen the Enterprise Growth Business over the medium to long term, we conducted a review of our support areas across the entire Creator Growth business and evaluated fields that could contribute more significantly to future profitability and business synergies.

As a result, we found that for some of the creators we had been supporting, synergies with other businesses, particularly the Enterprise Growth Business, were limited from the perspective of each region's owned characteristics and content attributes. Additionally, there were cases where, even if they were generating revenue at present, medium-term revenue growth potential was low. Furthermore, for some creators, we decided to discontinue support based on considerations such as content quality and brand compatibility.

As a result, the number of supported creators decreased from 2,101 in the third quarter of 2025 to 1,237 in the fourth quarter. On the other hand, the human and operational resources freed up by this have been reallocated to areas with high synergy potential with Enterprise Growth Business and high revenue expansion potential, such as providing support for creators with high affinity for brands and products who can contribute directly to commerce revenue generation, and the social commerce area, including live commerce.

With this reorganization of support areas, in fiscal year 2026, the Creator Growth Business alone is expected to experience a negative impact of approximately 500 million yen in operating profit due to revenue decline, but this impact is already factored into our financial forecast. On the other hand, we believe that the synergies created by concentrating resources on the Enterprise Growth Business, together with the stabilization and profitability improvements within the Creator Growth Business as it refocuses on priority growth areas, will bring medium- to long-term positive effects that exceed this.

Regarding the creators for whom our support has ended, the transition has already been completed, and at this point, we do not plan to make additional changes for similar reasons. From fiscal year 2026 onwards, we will proceed with business operations that balance profitability and growth, centering on the aforementioned priority areas after the reorganization.

Regarding the Creator Growth Business in fiscal year 2025, and as a result of changes in the external environment, gross profit was 2.64 billion yen, a decrease of 22.5% year-over-year.

In light of this situation, to strengthen the Enterprise Growth Business over the medium to long term, we conducted a review of our support areas across the entire Creator Growth business and evaluated fields that could contribute more significantly to future profitability and business synergies.

As a result, we found that for some of the creators we had been supporting, synergies with other businesses, particularly the Enterprise Growth Business, were limited from the perspective of each region's owned characteristics and content attributes. Additionally, there were cases where, even if they were generating revenue at present, medium-term revenue growth potential was low. Furthermore, for some creators, we decided to discontinue support based on considerations such as content quality and brand compatibility.

As a result, the number of supported creators decreased from 2,101 in the third quarter of 2025 to 1,237 in the fourth quarter. On the other hand, the human and operational resources freed up by this have been reallocated to areas with high synergy potential with Enterprise Growth Business and high revenue expansion potential, such as providing support for creators with high affinity for brands and products who can contribute directly to commerce revenue generation, and the social commerce area, including live commerce.

With this reorganization of support areas, in fiscal year 2026, the Creator Growth Business alone is expected to experience a negative impact of approximately 500 million yen in operating profit due to revenue decline, but this impact is already factored into our financial forecast. On the other hand, we believe that the synergies created by concentrating resources on the Enterprise Growth Business, together with the stabilization and profitability improvements within the Creator Growth Business as it refocuses on priority growth areas, will bring medium- to long-term positive effects that exceed this.

Regarding the creators for whom our support has ended, the transition has already been completed, and at this point, we do not plan to make additional changes for similar reasons. From fiscal year 2026 onwards, we will proceed with business operations that balance profitability and growth, centering on the aforementioned priority areas after the reorganization.

Please explain in detail the factors driving the significant growth of the D2C/E-commerce business.

Disclosed on November 14, 2025 (Partially updated)

The D2C/E-commerce business is divided into the Creator D2C/E-commerce business and the Enterprise D2C/E-commerce business.

The Creator D2C/E-commerce business is achieving growth by concentrating resources on high-profit brands, while the number of brands handled has remained stable. Strong performance from the fitness brand "LÝFT" and merchandise brands by managed talents such as "TAKESHITA PARADISE" is driving the growth of this business segment.

In the Enterprise D2C/E-commerce business, the number of brands is increasing, mainly in Southeast Asia. When the business began in 2022, we only offered a single solution, "AnyLogi," and our main client base consisted of small-scale clients. However, we are now focusing on acquiring and deepening relationships with large-scale clients, such as global brands. We have also significantly expanded our solution offerings, moving from providing a single solution to supporting operations for high-demand solutions like live commerce and assisting with expansion into multiple countries and marketplaces. This one-stop, end-to-end support structure has become a major factor in being chosen by large-scale clients.

As a result, we achieved high growth in Southeast Asia and Japan. The natural attrition from the expiration of contracts with small-scale clients has run its course, and the number of brands has returned to a net increase. Concurrently, due to the rising proportion of large-scale clients, revenue per brand has reached a record high.

The D2C/E-commerce business is divided into the Creator D2C/E-commerce business and the Enterprise D2C/E-commerce business.

The Creator D2C/E-commerce business is achieving growth by concentrating resources on high-profit brands, while the number of brands handled has remained stable. Strong performance from the fitness brand "LÝFT" and merchandise brands by managed talents such as "TAKESHITA PARADISE" is driving the growth of this business segment.

In the Enterprise D2C/E-commerce business, the number of brands is increasing, mainly in Southeast Asia. When the business began in 2022, we only offered a single solution, "AnyLogi," and our main client base consisted of small-scale clients. However, we are now focusing on acquiring and deepening relationships with large-scale clients, such as global brands. We have also significantly expanded our solution offerings, moving from providing a single solution to supporting operations for high-demand solutions like live commerce and assisting with expansion into multiple countries and marketplaces. This one-stop, end-to-end support structure has become a major factor in being chosen by large-scale clients.

As a result, we achieved high growth in Southeast Asia and Japan. The natural attrition from the expiration of contracts with small-scale clients has run its course, and the number of brands has returned to a net increase. Concurrently, due to the rising proportion of large-scale clients, revenue per brand has reached a record high.

Please tell us about the future growth strategy and revenue outlook for the Creator Growth Business.

Disclosed on July 2, 2025 (Partially updated)

Revenue from the Creator Growth Business is primarily classified into the following three areas:

1. Creator support centered on long-form video content

2. Creator support centered on short-form video content

3. Support for talents and artists activities other than video creators

Until the first half of 2023, 1. was the main focus, but from the second half of 2023 onward, 2. has grown significantly in addition to that, and currently 3. is experiencing growth. Following the changes in the external environment in March 2025, we have downsized and withdrawn from the short-form video domain 2. However, this has no impact on the other areas of the Creator Growth business, and we expect to maintain stable growth over the medium to long term.

In particular, to promote diversification of our revenue model, we are actively strengthening areas included in 3., such as talent and artist management, event planning, merchandise production and sales, and game production utilizing IP. These new initiatives are expected to become important pillars driving future business growth. As a concrete example, our group produced short drama channel 'shunkan seju' surpassed 60,000 TikTok followers in three months from launch, and tie-up projects are also progressing smoothly. Additionally, we have established a new label, "MUNI," which specializes in live commerce within the beauty and lifestyle sectors. Through this label, we will provide comprehensive support to our affiliated creators, from training and providing a live-streaming environment to securing advertising and event appearances.

Furthermore, within the overall creator economy market, diversification of monetization methods such as merchandise sales and fan communication is advancing, and we expect continued growth in market size. Globally, the creator economy market is predicted to grow at an annual average rate of 22.7% (1), and against this backdrop of market expansion, our business can be expected to continue steady growth. Additionally, there is significant potential for AI utilization in the creator support area, and we believe we can leverage our strengths in this regard as well.

Of note, the Creator Growth Business accounts for 18% of our group's total gross profit (fiscal year ending December 2024 results), and there have been no changes to the growth prospects or business environment for our core businesses, which since our foundation have been marketing and the D2C/EC business for enterprise clients. We will continue to aim for robust growth in these core businesses, driven by the strong demand in the Asian market.

(1) Source: Coherent Market Insights, compound annual growth rate for the global creator economy market from 2025 to 2032

Revenue from the Creator Growth Business is primarily classified into the following three areas:

1. Creator support centered on long-form video content

2. Creator support centered on short-form video content

3. Support for talents and artists activities other than video creators

Until the first half of 2023, 1. was the main focus, but from the second half of 2023 onward, 2. has grown significantly in addition to that, and currently 3. is experiencing growth. Following the changes in the external environment in March 2025, we have downsized and withdrawn from the short-form video domain 2. However, this has no impact on the other areas of the Creator Growth business, and we expect to maintain stable growth over the medium to long term.

In particular, to promote diversification of our revenue model, we are actively strengthening areas included in 3., such as talent and artist management, event planning, merchandise production and sales, and game production utilizing IP. These new initiatives are expected to become important pillars driving future business growth. As a concrete example, our group produced short drama channel 'shunkan seju' surpassed 60,000 TikTok followers in three months from launch, and tie-up projects are also progressing smoothly. Additionally, we have established a new label, "MUNI," which specializes in live commerce within the beauty and lifestyle sectors. Through this label, we will provide comprehensive support to our affiliated creators, from training and providing a live-streaming environment to securing advertising and event appearances.

Furthermore, within the overall creator economy market, diversification of monetization methods such as merchandise sales and fan communication is advancing, and we expect continued growth in market size. Globally, the creator economy market is predicted to grow at an annual average rate of 22.7% (1), and against this backdrop of market expansion, our business can be expected to continue steady growth. Additionally, there is significant potential for AI utilization in the creator support area, and we believe we can leverage our strengths in this regard as well.

Of note, the Creator Growth Business accounts for 18% of our group's total gross profit (fiscal year ending December 2024 results), and there have been no changes to the growth prospects or business environment for our core businesses, which since our foundation have been marketing and the D2C/EC business for enterprise clients. We will continue to aim for robust growth in these core businesses, driven by the strong demand in the Asian market.

(1) Source: Coherent Market Insights, compound annual growth rate for the global creator economy market from 2025 to 2032

What kind of business opportunity does the launch of TikTok Shop in Japan represent for your company? Please tell us about your specific initiatives.

Disclosed on July 2, 2025 (Partially updated)

The launch of TikTok Shop in Japan represents an extremely significant business opportunity for our company, and we believe we can establish a leading position in the social commerce area in Japan.

Our company has accumulated extensive experience and expertise overseas, particularly in Southeast Asian markets. For example, we have supported major food manufacturers in expanding sales on TikTok Shop in Indonesia, and in Thailand we have been recognized as a top-tier "Prime Partner" by TikTok Shop, demonstrating our leading social commerce support track record in Asia. These achievements are supported by our specialized solution suite in this field, including our internally developed EC management tool "AnyX" and our generative AI-powered live commerce tool "AnyLive." Furthermore, in April of this year, we announced the M&A of Vibula, a prominent live commerce company in Vietnam, strengthening our organizational structure and operational know-how while accelerating global expansion.

Based on this global foundation, we are also actively advancing specific initiatives for the Japanese market. On the product side, we announced in June 2025 that our EC management tool "AnyX" and logistics management tool "AnyLogi" would begin API integration with TikTok Shop Japan. Additionally, our live commerce tool "AnyLive" has newly added Japanese language support, expanding compatible languages to 8 languages, enabling live commerce deployment across multiple languages and regions. AnyLive is also now equipped with a new function for collecting and analyzing data during live broadcasts.

Furthermore, as we recently announced, our company has been certified as an official TikTok Shop partner in Japan, in addition to our existing partnerships in Indonesia, Malaysia, the Philippines, Thailand, and Vietnam. We have established a one-stop support system for TikTok Shop that covers everything from initial planning and account management to creator collaborations, advertising, live streaming, and logistics support. By leveraging our expertise, platform, and network cultivated in Southeast Asia, we will further support the growth of brands, creators, and sellers in the Japanese market through our TikTok Shop operational support.

In terms of business development, we are already receiving numerous inquiries from clients. In anticipation of the Japanese launch of "TikTok Shop," we announced the start of providing support services for brand companies, and from May to June, we jointly held multiple seminars with TikTok for Business regarding TikTok Shop utilization. We have attracted 50 to 100 participants each time, receiving very high interest from the market and specific consultations, and we have already begun closing the deals. Our policy is to prioritize establishing market share in the Japanese market first, and steadily develop this into a medium to long-term business pillar.

The launch of TikTok Shop in Japan represents an extremely significant business opportunity for our company, and we believe we can establish a leading position in the social commerce area in Japan.

Our company has accumulated extensive experience and expertise overseas, particularly in Southeast Asian markets. For example, we have supported major food manufacturers in expanding sales on TikTok Shop in Indonesia, and in Thailand we have been recognized as a top-tier "Prime Partner" by TikTok Shop, demonstrating our leading social commerce support track record in Asia. These achievements are supported by our specialized solution suite in this field, including our internally developed EC management tool "AnyX" and our generative AI-powered live commerce tool "AnyLive." Furthermore, in April of this year, we announced the M&A of Vibula, a prominent live commerce company in Vietnam, strengthening our organizational structure and operational know-how while accelerating global expansion.

Based on this global foundation, we are also actively advancing specific initiatives for the Japanese market. On the product side, we announced in June 2025 that our EC management tool "AnyX" and logistics management tool "AnyLogi" would begin API integration with TikTok Shop Japan. Additionally, our live commerce tool "AnyLive" has newly added Japanese language support, expanding compatible languages to 8 languages, enabling live commerce deployment across multiple languages and regions. AnyLive is also now equipped with a new function for collecting and analyzing data during live broadcasts.

Furthermore, as we recently announced, our company has been certified as an official TikTok Shop partner in Japan, in addition to our existing partnerships in Indonesia, Malaysia, the Philippines, Thailand, and Vietnam. We have established a one-stop support system for TikTok Shop that covers everything from initial planning and account management to creator collaborations, advertising, live streaming, and logistics support. By leveraging our expertise, platform, and network cultivated in Southeast Asia, we will further support the growth of brands, creators, and sellers in the Japanese market through our TikTok Shop operational support.

In terms of business development, we are already receiving numerous inquiries from clients. In anticipation of the Japanese launch of "TikTok Shop," we announced the start of providing support services for brand companies, and from May to June, we jointly held multiple seminars with TikTok for Business regarding TikTok Shop utilization. We have attracted 50 to 100 participants each time, receiving very high interest from the market and specific consultations, and we have already begun closing the deals. Our policy is to prioritize establishing market share in the Japanese market first, and steadily develop this into a medium to long-term business pillar.

Please tell us about the impact on your business from changes in US tariff policies and international situation.

Disclosed on May 14, 2025

As our business development activities and sales revenue in the US market are limited, we expect the direct impact of US tariff policies to be extremely limited. While there could be indirect effects from the risk of economic deterioration in the global economy, at present, we do not see specific signs such as reduction in marketing budgets by customers in the Asian market, and the deterioration of economic sentiment has not particularly materialized.

In our Marketing business, we have a diverse customer base of over 1,000 companies annually, and risk diversification has progressed with the revenue contribution ratio of the largest customer being less than 5.0%, so we view the impact of economic fluctuations on overall performance as limited.

On the other hand, trade within Asia may be further activated due to the impact of global trade friction, and the importance of the Asian market may be reassessed. We view this environment as a new business opportunity and will leverage our strength in having a flexible business foundation spanning multiple countries to demonstrate cross-border responsiveness and enhance our competitive advantage even amid market changes.

We will continue to develop flexible strategies while monitoring geopolitical risks and changes in the international situation, aiming for medium to long-term growth centered on the Asian market.

As our business development activities and sales revenue in the US market are limited, we expect the direct impact of US tariff policies to be extremely limited. While there could be indirect effects from the risk of economic deterioration in the global economy, at present, we do not see specific signs such as reduction in marketing budgets by customers in the Asian market, and the deterioration of economic sentiment has not particularly materialized.

In our Marketing business, we have a diverse customer base of over 1,000 companies annually, and risk diversification has progressed with the revenue contribution ratio of the largest customer being less than 5.0%, so we view the impact of economic fluctuations on overall performance as limited.

On the other hand, trade within Asia may be further activated due to the impact of global trade friction, and the importance of the Asian market may be reassessed. We view this environment as a new business opportunity and will leverage our strength in having a flexible business foundation spanning multiple countries to demonstrate cross-border responsiveness and enhance our competitive advantage even amid market changes.

We will continue to develop flexible strategies while monitoring geopolitical risks and changes in the international situation, aiming for medium to long-term growth centered on the Asian market.

Will there be no expansion into new countries or regions in the future?

Disclosed on April 2, 2025

While we are constantly considering expansion into new markets, our current focus is on prioritizing business penetration in the Asian, Indian, and Middle Eastern markets, where we believe there are sufficient opportunities and room for growth. For the time being, this is a phase of further deepening business in existing markets, and even if we do expand into Western or other emerging markets, we anticipate starting with a limited approach, such as establishing sales offices first.

On the other hand, in the medium to long term, we will carefully consider the possibility of expansion into regions outside Asia, leveraging the networks, customer base, and business models developed, while taking into account business resources.

Regarding the Chinese market, we do not currently anticipate aggressive domestic expansion in China, and the policy for China-related business is to focus on supporting outbound or inbound demand from Chinese companies.

While we are constantly considering expansion into new markets, our current focus is on prioritizing business penetration in the Asian, Indian, and Middle Eastern markets, where we believe there are sufficient opportunities and room for growth. For the time being, this is a phase of further deepening business in existing markets, and even if we do expand into Western or other emerging markets, we anticipate starting with a limited approach, such as establishing sales offices first.

On the other hand, in the medium to long term, we will carefully consider the possibility of expansion into regions outside Asia, leveraging the networks, customer base, and business models developed, while taking into account business resources.

Regarding the Chinese market, we do not currently anticipate aggressive domestic expansion in China, and the policy for China-related business is to focus on supporting outbound or inbound demand from Chinese companies.

Please tell us about the growth potential of 'AnyLive,' the new solution announced on September 25, 2024.

Disclosed on January 8, 2025

At the end of September 2024, we launched 'AnyLive,' a multilingual generative AI live commerce platform. In just a few months since its launch, we have acquired prominent clients including the 'evian' brand, known for bottled water and skincare products. In the case of the evian brand, we implemented hybrid streaming in the Thai market, combining AI models with human livestreamers, achieving 3.5 times higher revenue compared to conventional methods while reducing streaming costs by 90%.

In recent years, live commerce (an e-commerce sales solution that promotes purchases through live video streaming while introducing products and communicating with viewers in real-time) has become an important marketing method for EC sales in Southeast Asia. However, live streaming faces limitations in broadcasting hours and frequency due to issues with human resources (livestreamers) and costs. 'AnyLive,' through its use of AI models for live commerce, not only enables easy support for seven Asian languages but also allows for 24-hour live commerce streaming, including off-hours when regular human-operated live commerce would not be available.

'AnyLive' operates as part of our D2C/EC segment, and since its announcement, it has been steadily increasing new client engagements as a major solution in our B2B EC business development efforts. While we believe live commerce requires a comprehensive approach, including not only AI models but also human livestreamers and collaborations with prominent influencers, we expect the importance of AI utilization to increase further. Currently, we are primarily supporting existing clients, but moving forward, we plan to accelerate the growth of our B2B EC support business by expanding the client base for 'AnyLive.

At the end of September 2024, we launched 'AnyLive,' a multilingual generative AI live commerce platform. In just a few months since its launch, we have acquired prominent clients including the 'evian' brand, known for bottled water and skincare products. In the case of the evian brand, we implemented hybrid streaming in the Thai market, combining AI models with human livestreamers, achieving 3.5 times higher revenue compared to conventional methods while reducing streaming costs by 90%.

In recent years, live commerce (an e-commerce sales solution that promotes purchases through live video streaming while introducing products and communicating with viewers in real-time) has become an important marketing method for EC sales in Southeast Asia. However, live streaming faces limitations in broadcasting hours and frequency due to issues with human resources (livestreamers) and costs. 'AnyLive,' through its use of AI models for live commerce, not only enables easy support for seven Asian languages but also allows for 24-hour live commerce streaming, including off-hours when regular human-operated live commerce would not be available.

'AnyLive' operates as part of our D2C/EC segment, and since its announcement, it has been steadily increasing new client engagements as a major solution in our B2B EC business development efforts. While we believe live commerce requires a comprehensive approach, including not only AI models but also human livestreamers and collaborations with prominent influencers, we expect the importance of AI utilization to increase further. Currently, we are primarily supporting existing clients, but moving forward, we plan to accelerate the growth of our B2B EC support business by expanding the client base for 'AnyLive.

Are there any risks you perceive for future performance or business operations?

Disclosed August 14, 2024

We operate in rapidly changing industries, so we constantly monitor changes in the industry and market. Additionally, as we expand globally, we also face geopolitical risks. However, our diversified business structure and revenue bases across various countries allow for risk distribution at the group level. Even with temporary changes in market conditions, we can expect stable growth in the Asian economy as a whole. Therefore, we believe that we have effective risk control as a group.

In business operations, more important points are recognizing the current situation regarding market changes in each country and implementing timely responses to these changes. For this, we believe that management teams in each country are crucial. While our company has diverse management members in each country, we believe that further strengthening of these country management teams is necessary to achieve higher growth in the medium to long term.

We operate in rapidly changing industries, so we constantly monitor changes in the industry and market. Additionally, as we expand globally, we also face geopolitical risks. However, our diversified business structure and revenue bases across various countries allow for risk distribution at the group level. Even with temporary changes in market conditions, we can expect stable growth in the Asian economy as a whole. Therefore, we believe that we have effective risk control as a group.

In business operations, more important points are recognizing the current situation regarding market changes in each country and implementing timely responses to these changes. For this, we believe that management teams in each country are crucial. While our company has diverse management members in each country, we believe that further strengthening of these country management teams is necessary to achieve higher growth in the medium to long term.

What is the revenue model for each business?

Disclosed on June 28, 2023 (Partially updated)

Our business is largely divided into the Enterprise Growth area and the Partner Growth area. In the Enterprise Growth area, we mainly provide growth support to corporate brands and the Brand Commerce area can be further sectioned into Marketing and D2C/EC businesses. The Marketing business provides offerings such as influencer marketing and digital marketing. The revenue model is one in which we receive marketing fees from corporate advertisers to implement marketing activities, and the cost of sales are payments to influencers and media (web media and mobile apps).

The D2C/EC business offers multiple solutions in the e-commerce value chain, including production, ecommerce management, and logistics. In the D2C (direct-to-consumer) business for creators, we have a product sales model, in which we hold inventory and earn revenue by selling D2C products together with creators. In the business of providing e-commerce support to corporate clients, there are multiple revenue models, including a sales-sharing model in which we receive a fixed percentage of the income generated from e-commerce sales, a model in which we provide individual solutions and receive a fixed monthly fee, and, a pay-as-you-go model in which we are compensated based on shipping fees, etc. (for AnyLogi, an inventory and logistics management solution).

In the Publisher Growth business for publishers operating web media and mobile applications, and the Creator Growth business for creators such as YouTubers and TikTokers, our primary revenue model is revenue sharing based on a fixed percentage of advertising revenue. For the revenue sharing model, we recognize advertising revenue received as gross amount and the payments to publishers and creators (other than the percentage of revenue sharing) are treated as cost of sales (whether we adopt the gross or net revenue recognition depends on the structure of contracts with publishers or creators, and the increase in gross profit margin which occurred in 2022 for the creator business was due to an increase in the proportion of contracts that are treated as net amount.). In addition, we also provide support to publishers for website/mobile app UX improvement, data analysis, and other services, and some of our offerings for a fixed fee.

Our business is largely divided into the Enterprise Growth area and the Partner Growth area. In the Enterprise Growth area, we mainly provide growth support to corporate brands and the Brand Commerce area can be further sectioned into Marketing and D2C/EC businesses. The Marketing business provides offerings such as influencer marketing and digital marketing. The revenue model is one in which we receive marketing fees from corporate advertisers to implement marketing activities, and the cost of sales are payments to influencers and media (web media and mobile apps).

The D2C/EC business offers multiple solutions in the e-commerce value chain, including production, ecommerce management, and logistics. In the D2C (direct-to-consumer) business for creators, we have a product sales model, in which we hold inventory and earn revenue by selling D2C products together with creators. In the business of providing e-commerce support to corporate clients, there are multiple revenue models, including a sales-sharing model in which we receive a fixed percentage of the income generated from e-commerce sales, a model in which we provide individual solutions and receive a fixed monthly fee, and, a pay-as-you-go model in which we are compensated based on shipping fees, etc. (for AnyLogi, an inventory and logistics management solution).

In the Publisher Growth business for publishers operating web media and mobile applications, and the Creator Growth business for creators such as YouTubers and TikTokers, our primary revenue model is revenue sharing based on a fixed percentage of advertising revenue. For the revenue sharing model, we recognize advertising revenue received as gross amount and the payments to publishers and creators (other than the percentage of revenue sharing) are treated as cost of sales (whether we adopt the gross or net revenue recognition depends on the structure of contracts with publishers or creators, and the increase in gross profit margin which occurred in 2022 for the creator business was due to an increase in the proportion of contracts that are treated as net amount.). In addition, we also provide support to publishers for website/mobile app UX improvement, data analysis, and other services, and some of our offerings for a fixed fee.

Are there any other companies operating in the same business as your company?

Disclosed on June 28, 2023

Our company provides a wide range of solutions primarily in the areas of e-commerce and marketing, 1 including brand building, production management, e-commerce site development and operation, marketing, and logistics management. We have expanded our operations to 13 markets across the region, which means that there are no direct competitors in the entire business. Even when considering individual business segments, there are fewer cases of competition in the entire region of development. Usually, in each country, there are local competitors in each respective business segment separately.

Furthermore, by leveraging the benefits of scaling through global business expansion, we have invested in technologies and data utilization, provided services across Asia through cross-border operations, and offered comprehensive support along the business value chain. This distinctive positioning has led to complementary relationships with local companies in various countries, resulting in numerous cases of collaboration rather than pure competition.

Since our establishment, we have consistently invested in data and products, and we have built a strong local network and organization in each Asian market. We believe that our business foundation provides us with a competitive advantage in the respective country-specific competitive environment. We aim to continue enhancing our unique value proposition and achieve further growth in the future.

Our company provides a wide range of solutions primarily in the areas of e-commerce and marketing, 1 including brand building, production management, e-commerce site development and operation, marketing, and logistics management. We have expanded our operations to 13 markets across the region, which means that there are no direct competitors in the entire business. Even when considering individual business segments, there are fewer cases of competition in the entire region of development. Usually, in each country, there are local competitors in each respective business segment separately.

Furthermore, by leveraging the benefits of scaling through global business expansion, we have invested in technologies and data utilization, provided services across Asia through cross-border operations, and offered comprehensive support along the business value chain. This distinctive positioning has led to complementary relationships with local companies in various countries, resulting in numerous cases of collaboration rather than pure competition.

Since our establishment, we have consistently invested in data and products, and we have built a strong local network and organization in each Asian market. We believe that our business foundation provides us with a competitive advantage in the respective country-specific competitive environment. We aim to continue enhancing our unique value proposition and achieve further growth in the future.

How the Company manage a multinational organization and multinational operation.

Disclosed on June 28, 2023

We have been operating in multiple countries since our establishment, and we have worked towards establishing a structure based on multinational operations. We have built a matrix organization based on two axes, country, and business. Country managers oversee operations in each country, including local teams, and are responsible for talent management, customer relations, and addressing issues specific to local markets. Regional leaders within the business axis focus on optimizing products and operations, tackling challenges that are common globally. This matrix group structure enables us to efficiently manage our business and organization.

We have also implemented a shared accounting system and CRM system throughout the company, including the companies we acquired, and have established an environment where earnings and KPI are managed in real time by business and by country, and weekly discussions are held with the head of each business in each country to review the progress and address issues faced by each business. In addition, we conduct monthly profit analysis by business unit for each country to identify businesses that require investment and businesses that need productivity improvement, and we have a system in place to respond and discuss in a timely manner.

The culture of the entire organization is very flat, and the country managers in each country work closely with other members of the group management team to improve operations in each country through mutual information sharing. In addition, for companies that have joined the group through M&A, we will promote full business integration, including organization and structure, and will establish a reporting line for each country's corporate team in both the regional and country manager's direction. We are also working to build a structure that will allow us to have more resolution and control over each country's business from the perspective of governance.

We have been operating in multiple countries since our establishment, and we have worked towards establishing a structure based on multinational operations. We have built a matrix organization based on two axes, country, and business. Country managers oversee operations in each country, including local teams, and are responsible for talent management, customer relations, and addressing issues specific to local markets. Regional leaders within the business axis focus on optimizing products and operations, tackling challenges that are common globally. This matrix group structure enables us to efficiently manage our business and organization.

We have also implemented a shared accounting system and CRM system throughout the company, including the companies we acquired, and have established an environment where earnings and KPI are managed in real time by business and by country, and weekly discussions are held with the head of each business in each country to review the progress and address issues faced by each business. In addition, we conduct monthly profit analysis by business unit for each country to identify businesses that require investment and businesses that need productivity improvement, and we have a system in place to respond and discuss in a timely manner.

The culture of the entire organization is very flat, and the country managers in each country work closely with other members of the group management team to improve operations in each country through mutual information sharing. In addition, for companies that have joined the group through M&A, we will promote full business integration, including organization and structure, and will establish a reporting line for each country's corporate team in both the regional and country manager's direction. We are also working to build a structure that will allow us to have more resolution and control over each country's business from the perspective of governance.

Is there any seasonality in your business?

Disclosed on April 13, 2023

On page 40 of the "Business Strategies and Growth Opportunities" document disclosed on March 29, 2023, the first quarter of the year (January-March) is expected to be a low season.

The first quarter has fewer business days and operating days than other quarters due to the New Year vacation and Lunar New Year vacations, etc. Many overseas companies (corporate customers) close their books in December and concentrate their marketing investments at the end of the fiscal year, so they often do not actively conduct marketing activities during January and Feburary. As a result, earnings, especially in our Marketing and Partner Growth businesses, tend to remain at lower levels compared to the preceding quarter. In Japan, March is the end of the fiscal year for many companies, which increases marketing spending, but January and February are also low seasons in Japan, and the Company has larger overseas businesses than Japan, resulting in the first quarter of the year being a low season.

The second (April-June) and third (July-September) quarters are not particularly seasonal, but since our business is in a growth stage, sales and gross profit are expected to be higher in the third quarter than in the second quarter.

The fourth quarter (October-December) is a high season for all businesses, as marketing activities and e-commerce sales increase for Diwali, India's biggest festival in October-November, and Christmas in December, and many overseas companies have a December fiscal year end and tend to concentrate their marketing spending at the end of the fiscal year.

The quarterly distribution of gross profit for the fiscal year ending December 2022, was 20% for the first quarter, 24% for the second quarter, 25% for the third quarter, and 31% for the fourth quarter, indicating that the contribution to earnings increases towards the latter half of the year due to both seasonality and our business growth. We expect the same seasonality and trend to continue in the fiscal year ending December 2023, and beyond.

On page 40 of the "Business Strategies and Growth Opportunities" document disclosed on March 29, 2023, the first quarter of the year (January-March) is expected to be a low season.

The first quarter has fewer business days and operating days than other quarters due to the New Year vacation and Lunar New Year vacations, etc. Many overseas companies (corporate customers) close their books in December and concentrate their marketing investments at the end of the fiscal year, so they often do not actively conduct marketing activities during January and Feburary. As a result, earnings, especially in our Marketing and Partner Growth businesses, tend to remain at lower levels compared to the preceding quarter. In Japan, March is the end of the fiscal year for many companies, which increases marketing spending, but January and February are also low seasons in Japan, and the Company has larger overseas businesses than Japan, resulting in the first quarter of the year being a low season.

The second (April-June) and third (July-September) quarters are not particularly seasonal, but since our business is in a growth stage, sales and gross profit are expected to be higher in the third quarter than in the second quarter.

The fourth quarter (October-December) is a high season for all businesses, as marketing activities and e-commerce sales increase for Diwali, India's biggest festival in October-November, and Christmas in December, and many overseas companies have a December fiscal year end and tend to concentrate their marketing spending at the end of the fiscal year.

The quarterly distribution of gross profit for the fiscal year ending December 2022, was 20% for the first quarter, 24% for the second quarter, 25% for the third quarter, and 31% for the fourth quarter, indicating that the contribution to earnings increases towards the latter half of the year due to both seasonality and our business growth. We expect the same seasonality and trend to continue in the fiscal year ending December 2023, and beyond.

About Financial Results and Performance

What is the expected quarterly breakdown of the full-year operating profit plan for the fiscal year 2026?

Disclosed on April 3, 2026

We project an operating profit of 3.06 billion yen for the fiscal year ending December 2026, representing a 70% YoY increase driven primarily by the growth of the Enterprise Growth business.

Our Group's financial results typically exhibit seasonality weighted toward the second half of the fiscal year, with profit levels being lowest in Q1 and progressively increasing toward Q4. The quarterly distribution of operating profit is projected to generally follow the sequence of Q1 < Q2 < Q3 < Q4. The three companies acquired through M&A and consolidated starting in January 2026 also exhibit a similar trend.

We anticipate that the effects of productivity improvements driven by business standardization and AI utilization on a Group-wide basis will contribute more significantly in the second half than in the earlier part of the fiscal year; taking these factors into consideration, we have formulated a plan weighted toward the second half.

We project an operating profit of 3.06 billion yen for the fiscal year ending December 2026, representing a 70% YoY increase driven primarily by the growth of the Enterprise Growth business.

Our Group's financial results typically exhibit seasonality weighted toward the second half of the fiscal year, with profit levels being lowest in Q1 and progressively increasing toward Q4. The quarterly distribution of operating profit is projected to generally follow the sequence of Q1 < Q2 < Q3 < Q4. The three companies acquired through M&A and consolidated starting in January 2026 also exhibit a similar trend.

We anticipate that the effects of productivity improvements driven by business standardization and AI utilization on a Group-wide basis will contribute more significantly in the second half than in the earlier part of the fiscal year; taking these factors into consideration, we have formulated a plan weighted toward the second half.

When and to what extent will the effects of AI-driven operational efficiency and productivity improvements be reflected in financial results?

Disclosed on April 3, 2026

For generative AI-driven efficiency improvements, we initiated global process standardization in FY2025 and will enter the phase of delivering concrete results from FY2026.

In the Marketing business domain, which involves multiple operational processes, we are implementing AI-driven automation and streamlining of tasks such as proposal development and reporting analysis. Previously, multiple staff were involved in the process from business negotiations through to proposal delivery, which resulted in prolonged lead times and inconsistent quality. Through AI, we are automating key workflows while continuing to leverage our proprietary data, thereby minimizing the areas requiring manual intervention. We believe this will enable fast, high-quality proposals free from reliance on individual expertise, significantly shortening lead times and improving win rates. This model, which allows sales representatives to focus on higher value-added activities, is currently being rolled out across our global offices. In addition, we are automating processes such as invoice processing and management accounting within our administrative departments, driving operational efficiency on a company-wide basis.

Regarding the impact on financial results, our initial plan for the fiscal year assumes a moderate level of headcount growth, excluding M&A. However, by leveraging AI, we aim to keep actual headcount additions well below planned levels, which represents an upside factor relative to budget. We anticipate a full-scale contribution to financial results from the second half of FY2026 onward, with productivity improvement effects becoming more pronounced toward the latter half of our medium-term target period through 2027.

For generative AI-driven efficiency improvements, we initiated global process standardization in FY2025 and will enter the phase of delivering concrete results from FY2026.

In the Marketing business domain, which involves multiple operational processes, we are implementing AI-driven automation and streamlining of tasks such as proposal development and reporting analysis. Previously, multiple staff were involved in the process from business negotiations through to proposal delivery, which resulted in prolonged lead times and inconsistent quality. Through AI, we are automating key workflows while continuing to leverage our proprietary data, thereby minimizing the areas requiring manual intervention. We believe this will enable fast, high-quality proposals free from reliance on individual expertise, significantly shortening lead times and improving win rates. This model, which allows sales representatives to focus on higher value-added activities, is currently being rolled out across our global offices. In addition, we are automating processes such as invoice processing and management accounting within our administrative departments, driving operational efficiency on a company-wide basis.

Regarding the impact on financial results, our initial plan for the fiscal year assumes a moderate level of headcount growth, excluding M&A. However, by leveraging AI, we aim to keep actual headcount additions well below planned levels, which represents an upside factor relative to budget. We anticipate a full-scale contribution to financial results from the second half of FY2026 onward, with productivity improvement effects becoming more pronounced toward the latter half of our medium-term target period through 2027.

How achievable is the FY2026 plan for the Enterprise Growth business?

Disclosed on April 3, 2026

The Enterprise Growth business consists of the Marketing business and the D2C/E-commerce business. For the current fiscal year, we project a 57% YoY increase in revenue and a 59% YoY increase in gross profit.

The Marketing business plan for the current fiscal year (revenue: up 33% YoY; gross profit: up 27% YoY) assumes a high level of growth relative to results in the second half of the previous fiscal year. We believe the slowdown in the growth rate during that period was primarily attributable to a strategic reallocation of resources to support the rapidly growing D2C/E-commerce business, rather than a deterioration in the market environment.